Switzerland Social Security System

Pension system beast-mode?

In the past couple of weeks we discussed Polish social security system, and compared it with some Western European countries.

Poland was deemed very good.

West Europe systems seemed quite bad.

We briefly touched on Switzerland, and today we dive deeper into it.

We’ll talk about:

Swiss Health Insurance system

Swiss pension and social security systems:

1st pillar

2nd pillar

3rd pillar

Lets go!

Health insurance

IMO, a good deal.

Private healthcare (going to a specialist and paying out of pockets) is quite expensive, as many other things in Switzerland. The quality is good, but, in terms of value for money, there’s better deals out there.

But

Health insurance is mandatory - costs ~300-600 eur/month:

The more you pay each month, the bigger the discounts on your healthcare expenses

Even if you pay the cheapest contribution amount (varies by city/canton, but roughly ~250-500 eur/month), you won’t spend more than 2500-3000 CHF/year in healthcare expenses (after that, insurance pays)

And with that, you get access to one of the best healthcare systems in the world.

It’s not cheap, it’s a little bit bureaucratic, the fact that the system is run by insurances can feel a bit nasty at times (like, when you’re sick, doctors and hospitals sometimes seem to care more about who’s gonna pay, rather than treating you).

But, it’s also:

Efficient (low wait times)

High quality: standards are high, clinics are modern and well-equipped, doctors and personnel are well-trained and well-staffed

So, all in all, I find the Swiss mandatory health insurance to be good value for money if you care about getting top-quality treatment - especially for the worst-case scenarios.

1st pillar

Mandatory first pillar of social security contributions.

Everyone who has an income in Switzerland - doesn’t matter if employed or self-employed - needs to pay this.

It pays for pension and some other stuff like disability insurance.

Most of your contributions on this pillar (~80%) pay for pensions.

Let’s check the returns you get on your 1st pillar contributions on your pension

Similar calculations that we’ve done for Poland (in depth) and Western Europe (briefly) here and here.

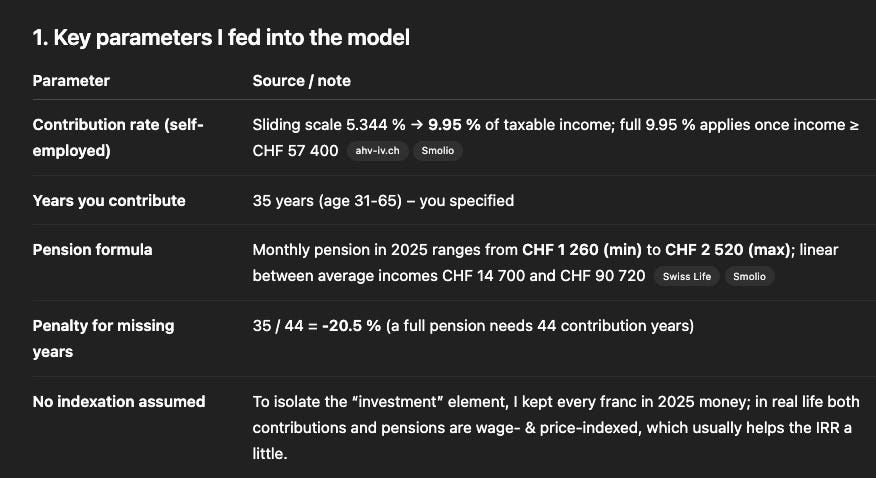

Assumptions

The number of years you contribute doesn’t really make a difference on the calculation of the returns, since both contributions and pension are indexed on a 44 years basis.

If you’re self-employed, you pay all the contributions yourself.

If you’re a full-time employee, you split it with your employer.

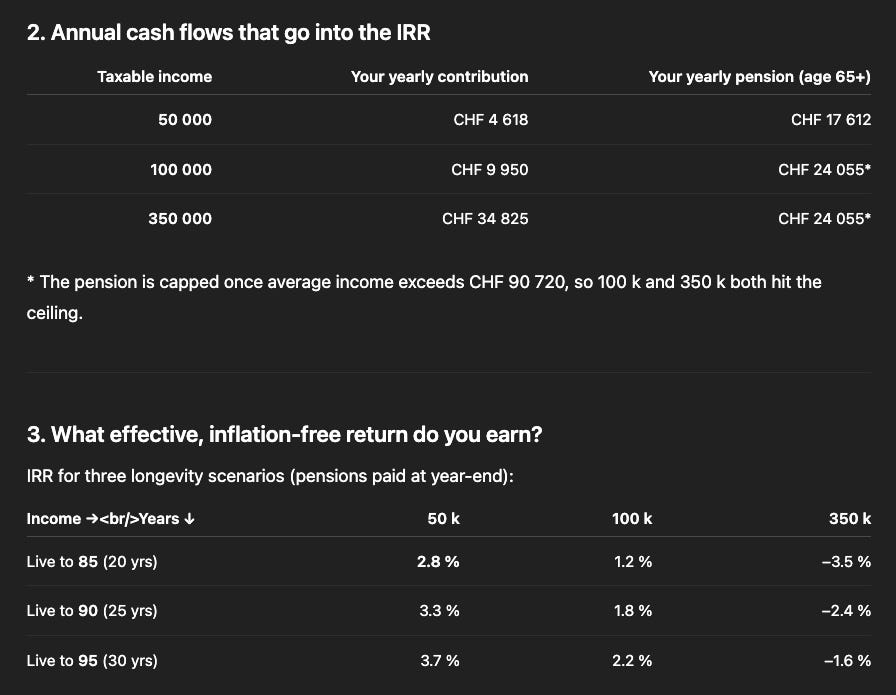

Returns for self-employed

Since the system gives you a pension within a range of roughly 15k-24k CHF per year, the less you earn (and, consequently, contribute), the higher the returns (high earners subsidise low earners).

The returns are not terrible, especially if you earn less than 100k CHF per year.

Also not that great, though.

Especially considering that if you’re working in Zurich and making less than 100k, you’re almost poor.

Compared to our previous analysis on Poland and other European countries:

The returns seem worse than in Poland

Better than most of the others (maybe worse than Czechia - haven’t investigated much)

More sustainable and less likely to get adjusted in the future than Polish one.

Also higher rate of the contribution goes to pension than in Poland (80% vs 60%)

So maybe, in the end, for low-earners, it’s similarly good (or even better) than the Polish system.

For high earners, it seems worse.

Important Note:

If you’re self-employed, you can usually structure things in a way where your income is not too high, so that you don’t pay too much and with bad returns on 1st pillar.

This can, for example, involve setting up an LLC where you hire yourself, and where you keep the income low-enough (ideally under 100k CHF/year), and you retain all the extra profits inside the company.

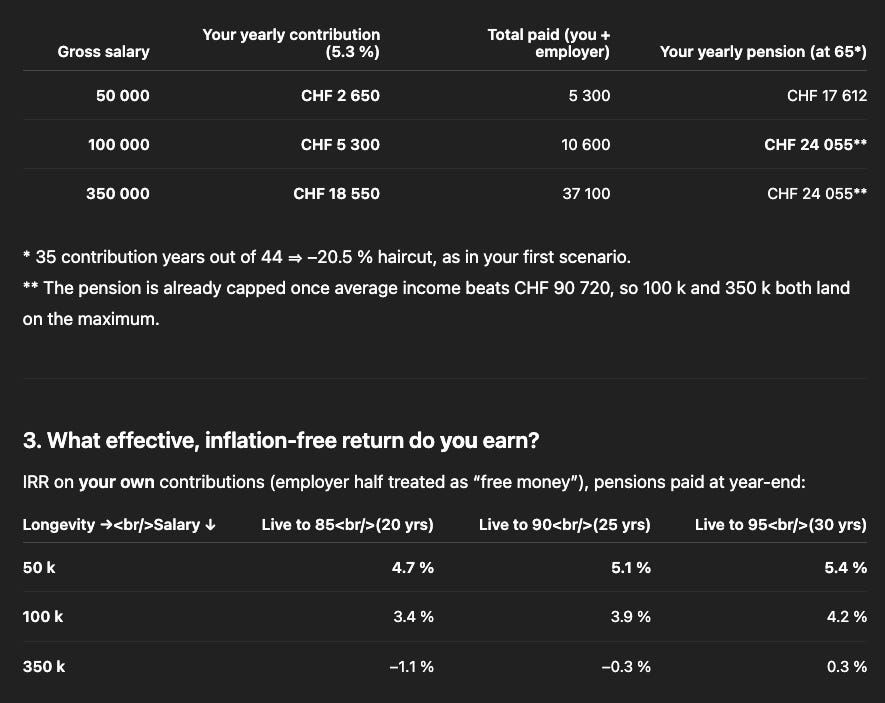

Returns for full-time employees

Much better!

Your employer pays half the money each month, but you get all the pension.

If you’re a low earner, it’s very good.

At 100k, still quite good.

Afterwards, so-so.

After 200k income, it’s already quite bad.

2nd pillar and 3rd pillar

They’re additional pension pillars you must/can contribute to, in addition the 1st pillar.

3rd pillar

Always elective: you don’t need to contribute if you don’t want

You can contribute 20% of your taxable income (up to a max of about 38k CHF/year) if you’re self-employed

You can only contribute up to 7k CHF a year if you’re employed

You can see it as a 401k: basically it’s tax deductible and you can invest the money however you like (at 0% capital gains)

2nd pillar

Mandatory if you’re an employee

It’s an additional pension scheme for people to have higher pensions than what the 1st pillar gives

You and your employer pay - or just you, if you’re self-employed

What you pay grows at roughly 1-2% each year, and, once you retire, you get each year 6.8% of what you’ve accumulated in the pillar

You can also cash out the contributions if you’re leaving Switzerland, starting a business or buying a house

Note: pensions in the 1st pillar range are not enough to get by in Switzerland, so you either spend your retirement abroad in cheaper locations, or you contribute to additional pillars like the 2nd pillar or the 3rd pillar (or draw from your own private funds)

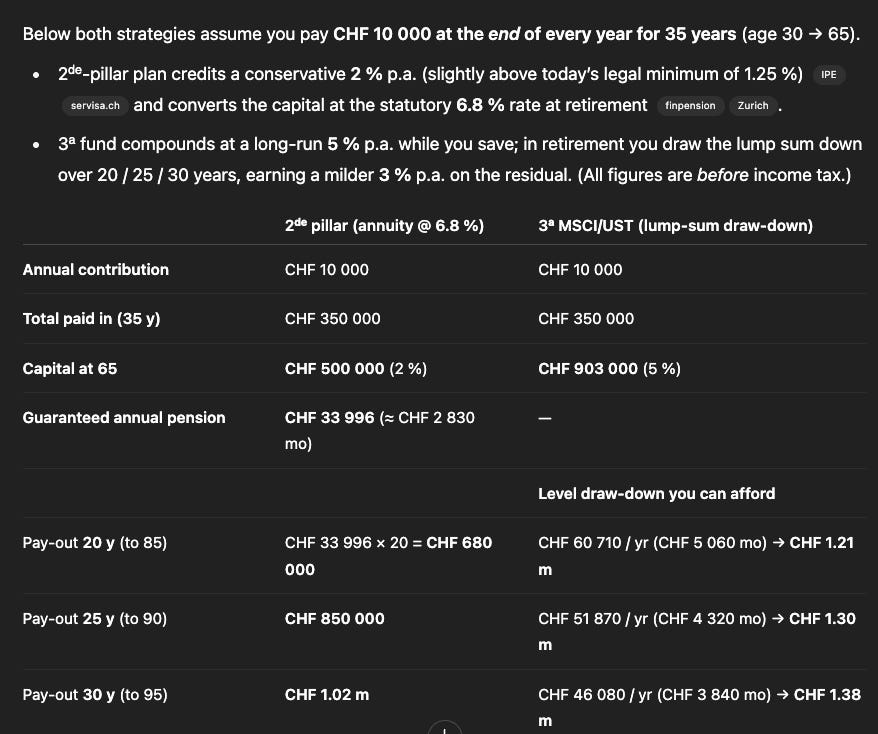

2nd pillar vs 3rd pillar

Self-employed people

Here I’m assuming a 5% market return for the 3rd pillar.

Assuming you invest in a mix of US treasuries (70%+), MSCI world Index (20%+), S&P500, etc. A conservative and low risk allocation.

The above calculation assumes you’ll contribute the same amount (10k CHF/year) onto each funds.

It shows how the 3rd pillar - basically, the market - is gonna pay more.

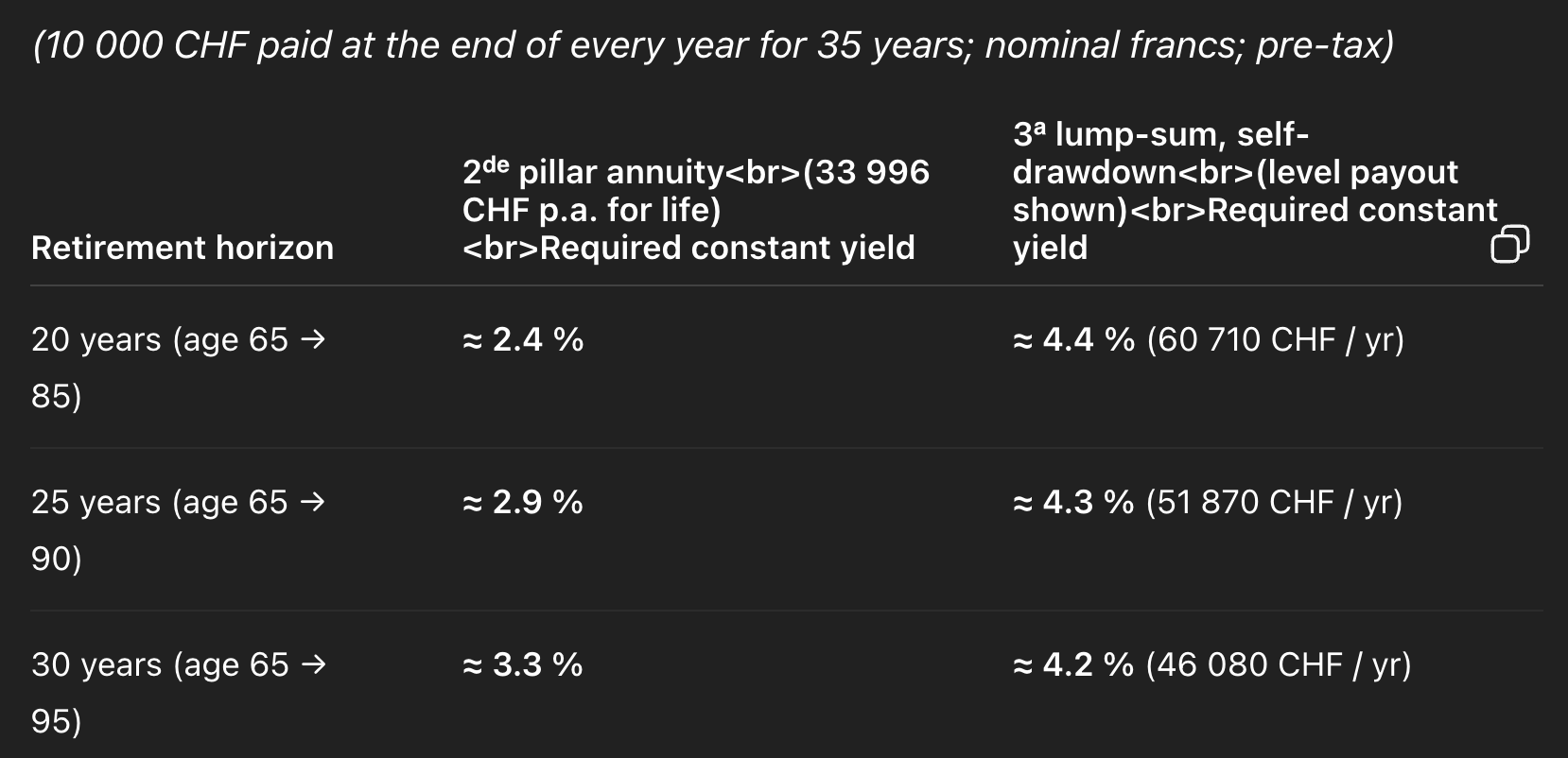

Here’s more detailed numbers on the returns:

The good thing about investing into the these pillars, instead of just investing into the market, is that you can deduct these sums from your taxable income - basically, it lowers your taxes.

Employees

The 2nd pillar is mandatory.

You split the yearly contributions with your employer.

It’s a good deal.

As you can see once again: like with the 1st pillar, these mandatory social security contributions make more sense if you’re employed.

If you’re self-employed, it’s probably better to limit your 1st and 2nd pillar contributions as much as you can, and focus on the 3rd pillar.

If you’re employed:

The 2nd pillar is gonna give you ~5% returns on your investments

= twice the returns you saw in the calculation for self-employed people above in the last screenshot (i.e. those 2.4%, 2.9% and 3.3% numbers)

So, in summary, contributing to your 2nd pillar while you’re employed it’s quite good.

If you ever move out from being an employee, an effective strategy could be to cash out the 2nd pillar contributions (especially if you’re far from retirement age), and invest it in the market (and get higher returns than these 1.5-2% ones).

As you get close to retirement, on the other hand, it could become again beneficial to contribute to the 2nd pillar, since this would imply building up a bucket of cash, on which you’ll get 6.8% dividends once you retire.

Note: if you’re employed and have to contribute to the 2nd pillar, you can still contribute to the 3rd pillar. But the max cap is lower: CHF 7’258 per year.

Conclusion

Switzerland is a good place to grow your Net Worth until and after retirement.

Pensions systems work well, have good returns overall, and are quite sustainable (unlike most systems in Europe).

Moreover, no capital gain tax on your other private investments.

This one can make a big difference over a long period of time. Back-of-the-envelope math:

If you’re investing a few hundred thousand euros at 4-8% yearly returns, having 0% capital gains or - lets say - 20% capital gains, will mean 400k-1M euros Net Worth difference over the course of a few decades.

Cost of living (CoL) is very high.

Especially as the CHF gets stronger - which will likely continue to be, given the uncertain times we live in / have ahead and the CHF role as safe asset class.

CoL can be reduced if you’re a remote worker and don’t spend all year in Switzerland.

CoL can be compensated if you’re working a local high-paying job (like Big Tech).

If you’re working the classic 100-130k CHF Zurich onsite job, the high CoL might - at least partially - outweigh the social security benefits we’ve discussed today.

Unless you naturally like living a frugal, nature-oriented, safe lifestyle.

Or unless you’re single and are only doing it for a few years to stack up some cash.

Or, if you appreciate any of the positive notes that Switzerland has - today, as well as in the future.

This last aspect will be the object of next week’s article.

Stay tuned if interested!

This article is brought to you by:

Euro Top Tech Jobs - The #1 resource for landing Top-Paying Tech roles in Europe:

4000+ top paying tech jobs in Europe from big tech companies, HFT firms and high-paying scale-ups.

Hundreds of jobs from 100+ fully-remote companies paying $100-600k per year.

Private guides - like this one - to help you land these jobs.

Six Figure Euro Engineer - Maximise your chances to boost your Tech Career in Europe, reducing time to success:

Work 1:1 with me (Nicola Amadio, author of this newsletter), and join the other engineers who were able to 10x their tech career in the past few months!